वापस जायें / Back

Revenue and Budget

Terminology

Budget – It is the estimate of revenue and expenditure of the Government for one year.

Budget deficit and Deficit Budget – Budget deficit is the difference between total receipts and total expenditure. Such a budget is called deficit budget. This deficit is made good by taking loans.

Deficit financing – When Government makes good the budget deficit by taking loan from the central bank of by issuing more currency notes, it is called deficit financing.

Revenue Deficit – When revenue expenditure is more than revenue income.

Fiscal Deficit – The difference between total revenue and total expenditure of the government is termed as fiscal deficit. It is an indication of the total borrowings needed by the government. Borrowings are not included in revenues. If borrowings and other liabilities are added to budget deficit, we get Fiscal deficits. Market borrowings, small savings, providend fund, external debt and budget deficit are included in it.

Primary deficit - refers to difference between fiscal deficit of the current year and interest payments on the previous borrowings.

Monetary deficit – This is the increase in currency issued by the central bank to make good the budgetary deficit of the Central Government. In other words it is the new currency issued every year. It represents the annual increase in the total credit given by the central bank to the Central Government.

Subsidy – Subsidy is a transfer of money from the government to an entity. It leads to a fall in the price of the subsidized product

Direct Tax – This is the tax on the income or assets of a person who pays it. Most important is personal income tax and corporate tax. Other direct taxes like wealth tax, gift tax, etc. have never been very important for the point of view of revenue earnings.

Indirect Tax - An indirect tax is a tax that is paid to the government by one entity in the supply chain, but it is passed on to the consumer as part of the price of a good or service. The consumer is ultimately paying the tax by paying more for the product. An indirect tax is shifted from one taxpayer to another. This includes taxes like GST.

Tax evasion – When tax is not paid by using illegal means.

Impact of Taxation – The burden on the first person who pays the tax is called impact of taxation. He can shift this burden on some other person as well. For example the burden of sales tax is shifted on the consumer by including it in the price of the product.

Incidence of Taxation – This is the burden of tax on the past person in the chain which cannot be shifted on any other person.

Funds of the Central Government

All receipts and expenditures of the Government are kept in three accounts as per the Constitution —

- Consolidated Fund of India

- Public Accounts

- Contingency Fund

Consolidated Fund – All revenues received by the Government by way of taxes like Income Tax, Central Excise, Customs and other receipts flowing to the Government in connection with the conduct of Government business i.e. Non-Tax Revenues are credited into the Consolidated Fund constituted under Article 266 (1) of the Constitution of India. Similarly, all loans raised by the Government by issue of Public notifications, treasury bills (internal debt) and loans obtained from foreign governments and international institutions (external debt) are credited into this fund. All expenditure of the government is incurred from this fund and no amount can be withdrawn from the Fund without authorization from the Parliament. There are two types of expenditure from the consolidated fund of India- charged and voted. Charged expenditures are those which Government of India is bound to make. No voting takes place on such expenditure in the Parliament. Voted are those expenditures on which voting takes place in the Parliament.

Following expenses are charged —

- Salary and allowances of the President.

- Salary and allowances of the chairman and vice chairman of the Rajya Sabha and speaker and deputy speaker of the Lok Sabha.

- Salary and allowances of the judges of Supreme Court.

- Salary and allowances of the judges of High Courts.

- Salary and allowances of the Comptroller and Auditor General of India.

- Salary and allowances of the chairman and members of the UPSC.

- Repayment of debts, for which Government of India is liable.

- Payments to be made in compliance of orders of courts.

Public Accounts – All public moneys received by or on behalf of the Government of India except those which are credited to the consolidated fund are entitled to the public account of India. These are basically debts not included in the consolidated fund. The receipts under Public Account do not constitute normal receipts of Government. Parliamentary authorization for payments from the Public Account is therefore not required. An example is the provided fund of employees.

Contingency Fund - Art 267(I) of the constitution provides that "Parliament may by law establish a Contingency Fund in the nature of an imprest to be entitled the Contingency Fund of India into which shall be paid from time to time such sums as may be determined by such law, and the said Fund shall be placed at the disposal of the President to enable advances to be made by him for the purposes of meeting unforeseen expenditure pending authorization of such expenditure by Parliament by law under Article 115 or Article 116".

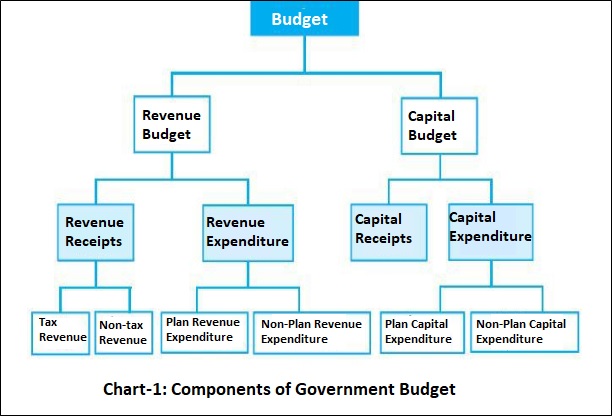

Components of Budget – Budget has two main components: (i) Revenue budget (ii) Capital budget.

Revenue budget – This includes all current receipts of the Government and the expenditure from them -

- Revenue receipts – These are those receipts of the Government which are not repayable. These can be classified into tax revenue and non-tax revenue –

- Tax Revenue – These are receipts from taxation. Taxes can be direct and indirect –

- Direct Tax – This is the tax on the income or assets of a person who pays it. Most important is personal income tax and corporate tax. Other direct taxes like wealth tax, gift tax, etc. have never been very important for the point of view of revenue earnings.

- Indirect Tax - An indirect tax is a tax that is paid to the government by one entity in the supply chain, but it is passed on to the consumer as part of the price of a good or service. The consumer is ultimately paying the tax by paying more for the product. An indirect tax is shifted from one taxpayer to another. This includes taxes like GST.

- Non-tax revenue – These include —

- Interest Receipts – These are interests on loans given by the Central Government to State Governments and other Government Organizations.

- Profit and dividend on investments of the Government – This is the income on investment in Government, semi-government and private companies by the Government.

- Fee on services provide by the Government.

- Grant-in-aid – This is grant-in-aid from foreign countries and International Organizations.

- Revenue Expenditure – Expenditure on things other then creation of physical or financial assets of the Government is called revenue expenditure. This includes expenditure on routine activities of Government Departments, payment of interest on loans taken by the Government, grants to the State Governments and other organizations, etc. Revenue expenditure is classified into plan and non-plan expenditure in the budget document -

- Plan revenue expenditure is related to plan schemes of the central government e.g. Five Year Plans, and central assistance to Union territories and states for their plans.

- Non-plan revenue expenditure – This mainly includes payment of interest, defense, salaries, pension, subsidies etc. The biggest component of non plan expenditure is payment of interest. The second largest component is defense expenditure.

Capital Budget – Capital account is the account of assets and liabilities of the Central Government –

- Capital Receipts – All receipts of the Government which create a liability of reduce the value of an asset are called capital receipts.

- Debt capital receipts – This is the public debt of the Government and mainly includes debts taken from the public, market debts, debts taken from the Reserve Bank of commercial banks on the basis of treasury bills, loans taken from foreign governments or International Organizations etc.

- Non-debts capital receipts – This includes post office small savings (Post office savings accounts, National Savings Certificates etc.), provident fund, net receipts from sale of shares of public sector undertakings (which is called disinvestment) etc.

- Capital Expenditure – This is the expenditure of the Government which results in the creation of physical or financial assets or reduces liabilities. Capital expenditure includes expenditure on land acquisition, construction, plant and machinery, investment in shares and loans given by the central government to state governments, union territories, and public undertakings etc. Capital expenditure is also classified into plan and non-plan in the budget document. Plan expenditure is related to the central assistance on plan schemes and non-plan expenditure is on routine social and financial services.

Reforms in New Economic Policy (1991) -

The then finance Minister Dr. Manmohan Singh announced the new economic policy in 1991 with the following main objectives -

- To make Indian economy market oriented to make it compatible with globalization.

- Reduce the rate of inflations and correct adverse balance of payments situation.

- Increase rate of economic growth and create an adequate foreign exchange reserve.

- Bring economic change for a market oriented economy by removing all unnecessary restrictions to achieve economic stability.

- To permit unrestricted flow of goods, services, human resources, and technology internationally.

- Increase the share of private companies in all sectors of the economy. The number of sectors reserved for public sector was reduced to three.

Important points of New Economic Policy:

- Liberalization –

- Self determination of interest rates by commercial banks.

- Enhancement of the limit of investment in Small and Marginal Industries (MSE).

- Freedom to import capital goods.

- Freedom for expansion and production to Industries.

- Abolition of Restrictive Trade Practices – Restrictions under MRTP Act, 1969 were reduced.

- Removal of Industrial Licensing and registration – However licensing is still required for railways, mining of atomic minerals and atomic energy.

- Privatization -

- Sale of Shares: Government of India sold shares of public undertakings, e.g. shares of Maruti Udyog Ltd. were sold and reached private hands.

- Disinvestment in PSUs: Government disinvested in PSUs which were in loss. Total disinvestment was to the tune of Rs 30000 crores.

- Minimization of Public Sector: Number of industries reserved for public sector was reduces from 17 to 3. These are - (a) Transport and railway, (b) Mining of atomic minerals and (c) Atomic energy.

- Globalization -

- Reduction in tariffs.

- Long term trade policy which was –

- Liberal

- Controls removed from foreign trade

- Open competition encouraged

- Partial convertibility of currency.

- Increase in equity limits of foreign investments.

Different types of Taxes

- Corporate Tax – On companies.

- Income Tax – On individual income.

- Excise – On manufacturing.

- Service Tax - On services.

- Wealth Tax – On moveable and immoveable property.

- Gift Tax – On the person accepting gifts.

Goods and Services Tax (GST)

Goods and Services Tax was introduced in India from 1st July 2017. This is an indirect tax. Many economists have called it the biggest reform since independence. This has replaced several taxes earlier imposed by the central and state Governments and has introduced a common indirect tax system for the entire country. This will help in developing a common market for India. Constitution was amended to bring this tax.

Earlier there was high tax rate to the tune of 30 to 35% on some goods. In some cases the tax rate was as high as 50%. After GST maximum tax rate has been reduced to 28%. Earlier there were 17 different types of taxes. Taxes like excise duty, service tax, Vat, entertainment tax luxury tax etc. have been removed. Now with GST tax is imposed on goods only at the place where they are sold. GST council has reduced tax rates on 66 types of products. There are only four slabs in GST - 5%, 12%, 18% and 28%.

Petrol, liquor and electricity have been kept out of GST.

Types of GST –

- Central GST (CGST) – recovered by the central government

- State GST (SGST) – recovered by the State Government for businesses within the state

- Integrated GST (IGST) – If a business is in 2 separate states then integrated GST will be recovered on it which will be recovered by the central government and distributed to both the states in equal proportion.

Nature of GST

GST is a value added tax which is a single tax from the stage of manufacture to consumption of goods and services. The benefit of input credit is given at every stage of value addition. At the last stage the consumer has to pay only the GST paid by the dealer.

Benefits of GST

- For commerce and Industry

- Simple compliance, transparent

- Uniformity in tax rates and structures

- Cascading of taxation has ended

- Reforms in competition

- Advantageous for manufacturers and exporters

- For central and State Governments

- Simple and easy administration

- Better control on misconduct

- Better revenue efficiency

- For consumers

- Proportional, single and transparent tax on the prices of goods and services

- Relief in the total tax burden

GST Council –

The chairman of this council is Finance Minister of India. Chief Ministers of all states are members. This council takes decisions on all important matters including tax rates of GST.